Tax Updates and Changes Related to COVID-19

Earlier this year, we shared our top tips for preparing for your 2019 income taxes. Well, the world has changed since then and so have tax laws.

While the new conditions for 2019 tax returns we shared previously will mostly still apply (click here to revisit those), there are a number of new provisions in effect as a result of the Covid-19 pandemic.

The most significant is Notice 2020-18, which defers the federal filing and payment deadlines for individuals, trusts and corporations from April 15 to July 15 with no limit and no penalty.

Here’s what you need to know about Notice 2020-18:

- This notice defers payments on 2019 balances due as well as 2020 1st Quarter estimated tax payments.

- There are no additional forms needed to delay filing and payment to July 15; you do not need to file an extension.

- If you are expecting a refund, you should file as soon as possible.

- Most states (including Ohio, Kentucky, Indiana and Illinois) and localities have conformed to the new July 15 deadline, but you should check with your state to be certain.

- Second quarter estimated tax payments are still due June 15, 2020 (this is actually before the 1st Quarter payment due date).

- The deadline for making a IRA or Roth IRA contribution as well as HSA contributions related to the 2019 tax return have been postponed July 15 as well.

For more information about the tax changes in effect, click here to visit details from the IRS.

Other significant tax implications are found in the $2 trillion CARES Act (Coronavirus Aid, Relief, and Economic Security Act):

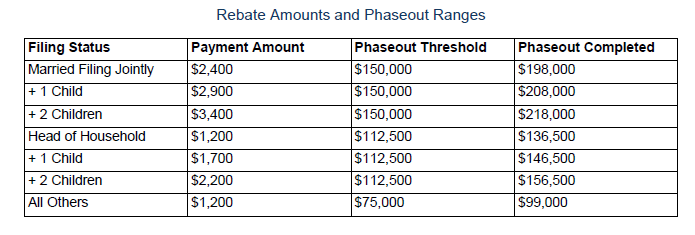

- Checks will be distributed to taxpayers under certain income limits.

U.S. residents who are not a dependent of another taxpayer

and have a work-eligible social security number will receive $1,200 ($2,400

married), with an additional $500 per dependent child. Payments will start to phase out for

individuals with adjusted gross incomes of more than $75,000 (150,000 married)

and those making more than $99,000 (198,000 married) will not qualify at all. The income ranges are based on your 2019

Adjusted Gross Income (AGI). If you have

not filed your 2019 income tax return, the payments will be based on your 2018

AGI. Depending on your AGI for 2018 or

2019, you should consider either accelerating or delaying the filing of your

2019 tax return. If your 2019 AGI was

much higher than your 2018 AGI, you should consider delaying the filing of your

2019 return and potentially receive a larger rebate check.

- RMDs are waived for 2020.

Required minimum distributions from an IRA, 401(k), 403(b), or an inherited IRA are waived for 2020. Therefore, you should strongly consider suspending a distribution from these accounts in 2020 and satisfy any cash needs from cash savings or other taxable or trust accounts. This is because distributions from these types of accounts are taxed at higher ordinary income tax rates, whereas distributions from taxable accounts can be made with a much lower tax burden. There are many considerations and planning opportunities that arise because of this provision and you should reach out to your Advisor for details. - Changes to charitable deductions now apply.

There is an allowance of up to $300 in charitable deductions for non-itemizing taxpayers beginning in tax year 2020. This is a new above-the-line deduction. In addition, the 50% adjusted gross income limitation on deductions for charitable contributions is suspended for 2020.

- The Paycheck Protection Program will distribute $350 Billion to small businesses.

The lending program, administered by the Small Business Administration, will provide eligible small businesses (with 500 or fewer employees) loans up to $10 million on favorable terms to help pay operational costs such as payroll, rent, and utilities. If a business satisfies certain conditions, portions of the loans are forgivable. Click here to learn more. There are also loans available to small businesses under the Economic Injury Disaster Loan program.

These are the most current tax changes as of the posting of this blog. With the ever-evolving circumstances related to the coronavirus pandemic, it is not out of the question that additional adjustments could come our way. We’ll continue working diligently to keep you informed of all the latest updates.

As always, these are my own opinions and suggestions, and they could change due to market or economic conditions, or other factors. It’s best to engage tax and legal counsel before taking action, as this commentary is not intended to serve as tax or legal advice.

When it comes to tax planning related to your investments, there’s always a lot to think about. Your Bartlett wealth advisor can help you consider your tax situation, alongside your other advisors, to determine which strategies make the most sense for you.